Posted on December, 16, 2024 at 09:37 am

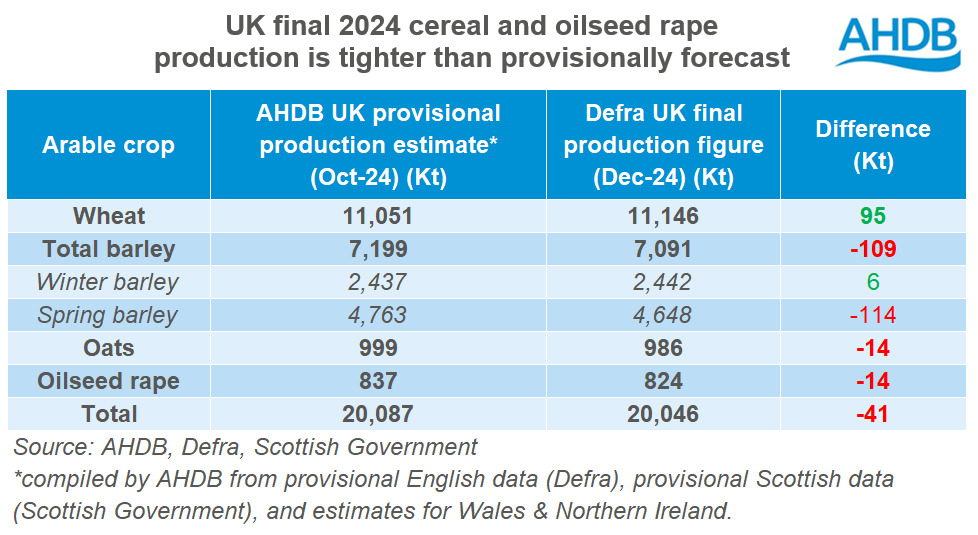

Earlier today, Defra released the final estimates for 2024 UK cereal and oilseed production. In order to provide an initial look at harvest 24, back in October, AHDB published “provisional” UK cereal and rapeseed production estimates following the release of Defra English and Scottish production figures. So, how do the final figures differ from our provisional estimates? And what does that mean for domestic supply and demand?

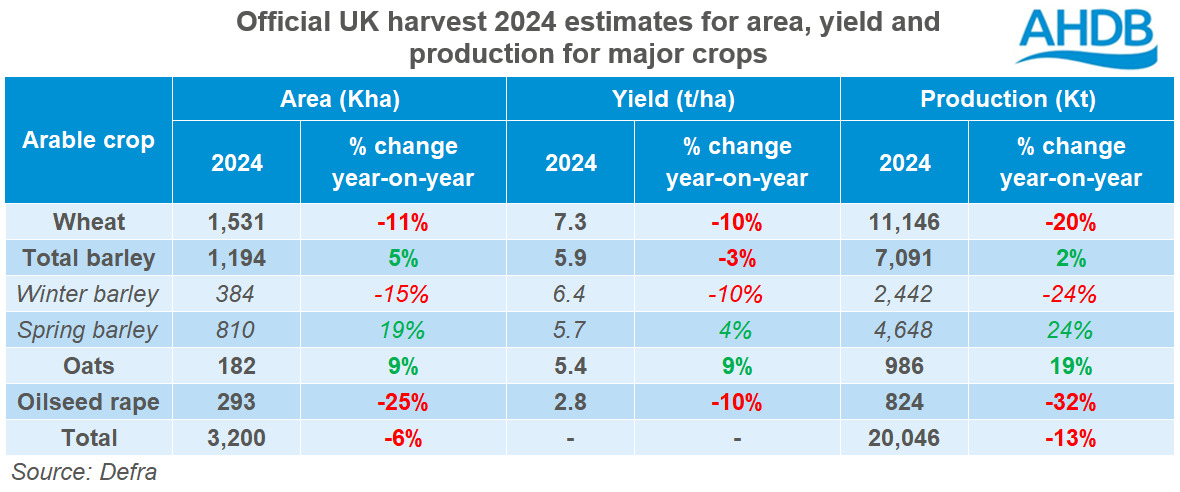

As is well known, following the wettest September – May on record (1,168 mm) last season, cereal and oilseed rape production in the UK was considerably challenged, particularly winter sown crops. While most spring crops fared better, according to today’s figures, total production of wheat, barley, oats and oilseed rape contracted by 13% on the year in 2024 to 20.0 Mt. This was in line with AHDB’s provisional estimate made in October, and remains the smallest harvest since 2020.

While most of the final crop estimates were relatively in line with AHDB’s provisional figures, the table below shows a larger decline in spring barley production than expected. This is due to smaller-than-expected yield estimates for the English and Scottish spring barley crops.

Defra’s slightly larger wheat crop estimate leads to a slight increase in wheat availability this season. With this new estimate, total availability of wheat would reach 16.88 Mt, up from 16.79 Mt using AHDB’s provisional figure. Using the latest consumption estimates, this therefore leads to a heavier balance of 2.81 Mt, and a greater surplus for either export or free stock of 1.255 Mt (just below the five-year average).

The downwards revision to the spring barley crop leads to a tighter barley balance of 1.94 Mt, and the surplus available for either export or free stock at 1.14 Mt (below the five-year average but in line with 2023/24).

A small cut to the oat estimate leaves the balance of UK oat supply and demand at 251 Kt. With exports currently estimated at 75 Kt, this would leave ending stocks at 176 Kt, above the five-year average and the heaviest since at least the turn of the century.

Overall, the final Defra production figures for harvest 2024 saw relatively minimal change from AHDB’s provisional estimates made in October.

The crop which saw the largest revision was barley, leaving a slightly tighter balance than initially expected. However as current export pace remains steady, we are unlikely to see much price reaction.

Focus has turned to what we can expect from harvest 2025. AHDB’s provisional Early Bird Survey forecasts an uptick in the planted wheat area, and a fall in barley area; the revised estimates using the final Defra figures are due to be published in the coming days. Our latest crop development report shows that the condition of crops is variable across GB, due to drilling time and regional weather changes.

The next AHDB UK cereal supply and demand estimates are scheduled for release in January 2025. These will include the 2024 Defra production estimates which were released today.

Source: AHDB